What are the Best Factors for Factor Investing?

What are the Best Factors for Factor Investing?

There are several models such as a widely used Fama-French three-factor model utilizing three factors, size of firm, book-to-market-values, and excess return on the market. But the correct answer to the question „What are the Best Factors for Factor Investing“ is that the “best” factors are constantly changing.

How do we know that?

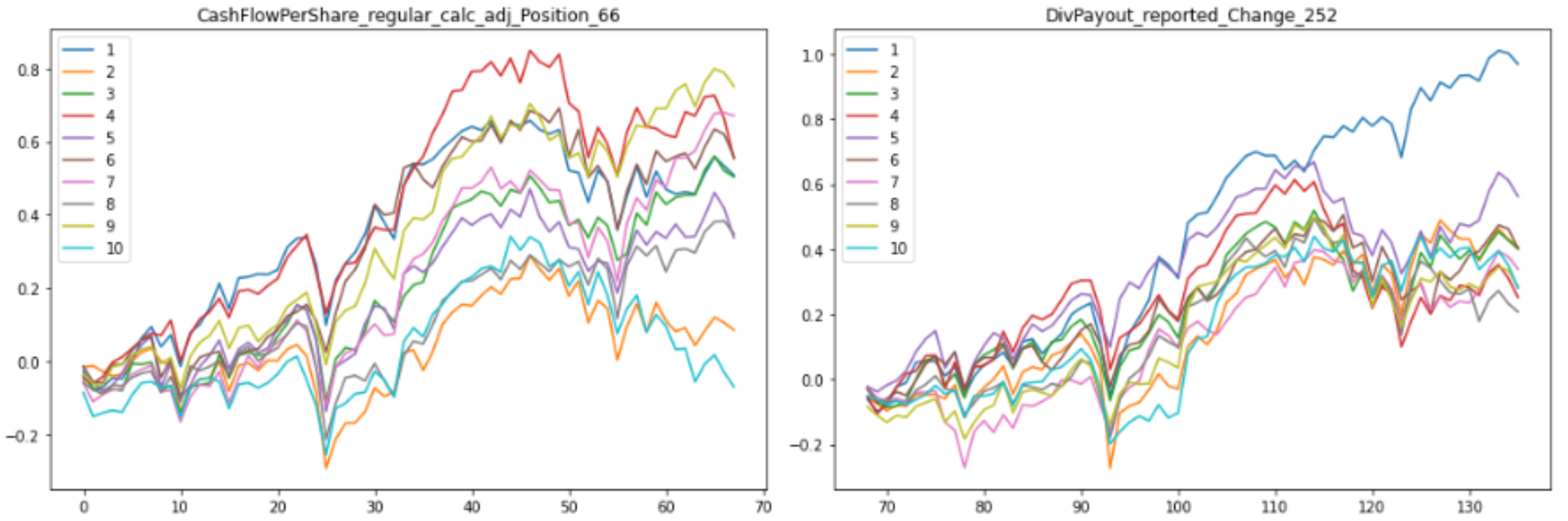

We have been running our own multi-factor asset pricing model (APM) since 2020, with satisfactory results. For the purposes of understanding how factors influence asset price, we have developed unique software. Our application tracks more than 3000 factors and provides revolutionary information about their behavior in the selected time period.

How to use information about the importance of the factor?

Analysts using factors for building their investment portfolios and products get valuable insight into the factor’s impact on real price moves. Very often the factors act exactly opposite to what theory and human reason say. And even on a very long-time series.

We provide not only information on how the factor influences the whole stock’s universe but also the impact on every single stock. So that analysts can see that for instance APPL stock is strongly affected by the selected factor. But on the other hand, the same factor has no real impact on the price moves of NVDA stock.

This is the pilot article. In the forthcoming weeks, we are going to deliver remarkable content providing you with information about the importance of factors being used for factor investing.

Methodological background

In finance, ‘factors’ usually refer to key attributes like size or value that explain investment risk and return. In this series of articles, we expand this term to include specific metrics like ‘Price-to-Earnings,’ using ‘factor’ and ‘specific characteristic’ interchangeably with the understanding that these attributes serve as representatives of factors that influence investment performance.

Stay tuned, sign up for our newsletter, follow us on LinkedIn, or let us know that you want to be our test user. We would love to give you a beta account credentials for our new software.

Find out more information in the follow-up article In Factor Investing Even the Best Can Lose – Data-Driven Insights into Factor-Based Analysis!