The utilization of big data and machine learning for investing is based on identifying and subsequently leveraging statistical advantages. For example, we have found a correlation between negative attention and stock price movements. However, translating this statistical advantage into real-world investing, or more specifically, building an investable portfolio, is another discipline that investors need to master.

In today’s post, we’ll take a closer look at the turnover of investment indicators. Turnover shows us the frequency of portfolio adjustments, i.e., how often and how much the portfolio needs adjusting. Translated into investors’ language, this determines the cost of fees and spreads, as well as the amount of time needed to manage the strategy.

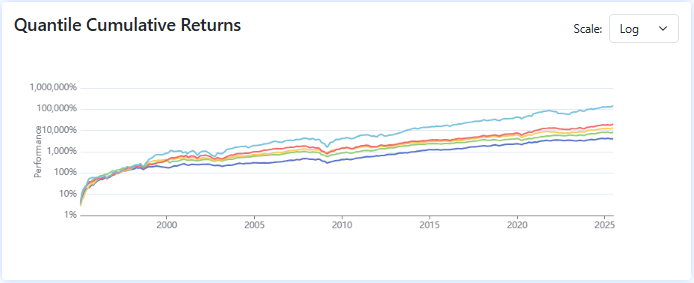

Return analysis of investment indicators

Our factor investing software assesses investment indicators/factors based on the performance of individual quantiles. For example, it shows how the 20 stocks with the lowest volatility (quantile 1) have performed within the S&P 100 index. The information obtained indicates which stocks to invest in or which indicators to use in our multifactor models.

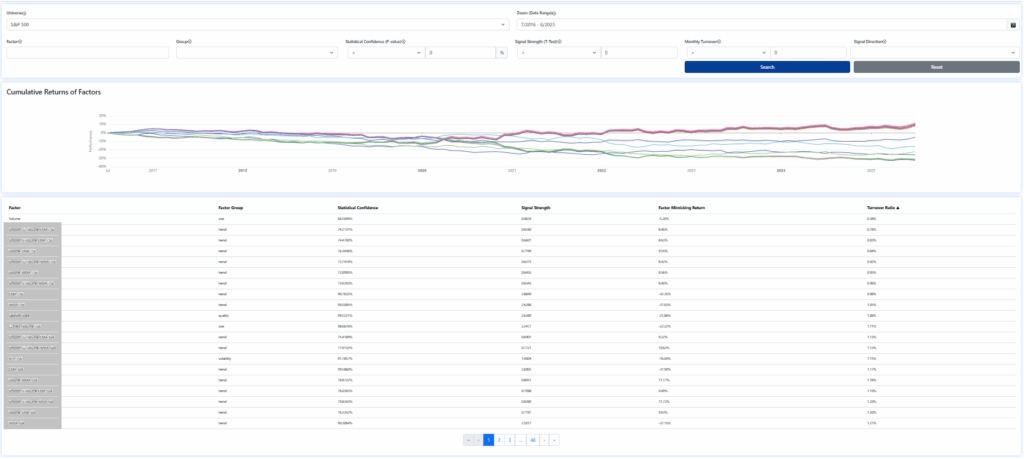

Turnover of investment indicators

However, finding an indicator with high performance using the above methodology does not necessarily mean that such an indicator will be suitable for our strategy/investment approach.

For example, momentum or volatility indicators are often associated with high stock turnover. The aforementioned Volatility 22 factor, which represents the fluctuation rate of a stock’s price over the past 22 trading days, is statistically significant, but it is associated with 50% stock turnover within quantiles.

In other words, when applying this factor in practice, half of the portfolio should be replaced every month. The factor, therefore, determines greater time and fee demands. This may be acceptable for swing traders who take advantage of other parameters of the factor. For investors with longer trading periods, the indicator is probably not very appropriate.

Turnover in factor analysis gives us the average monthly percentage change in the portfolio for the rebalancing period. TO 0% means that all stocks in the assessed quantiles remain unchanged. On the other hand, 100% means that all stocks are replaced at each rebalancing. In our case, the rebalancing period is one month. We have data from 1994 onwards where the desired periods can be zoomed in on.

Highest and lowest turnover

The lowest TO (less than 1%) within the S&P 500 over the previous ten years is observed for the size indicator Volume, which refers to the total number of shares that are traded for a particular stock during a specified time period. It serves as an indicator of investor interest and market activity. High trading volumes often suggest a change in investor sentiment and can trigger significant price movements, making it a vital tool for investors to identify potential investment opportunities or risks.

On the contrary, the biggest TO (more than 90%) can be observed in the momentum Smooth 5 Volume ROC 22 factor. This factor represents the rate of change in the smoothed 5-day trading volume over the past 22 days. This indicator reflects the momentum and velocity of volume changes, which can help investors understand the intensity of the trading activity and potential price movements.

For the detailed methodology, calculations, and charts, feel free to write to us at app@analyticalplatform.com. You can also review the indicators you are interested in with our Factor Investing software.

July 2, 2025, Jiří Fuchs, CCFR/Analytical Platform

Register today & enjoy one month

FREE trial of our application